")

")

- Home

- About Us

- Our Products

- KGF Equity Backed Guarantees

- Treasury Backed Guarantees

- ACTIVE SUPPORT PACKAGES(2023)

- EXPORT SUPPORT PACKAGE

- INVESTMENT SUPPORT PACKAGE

- SUPPORT PACKAGE FOR OPERATING EXPENSES

- INVESTMENT-PROJECT FINANCE SUPPORT PACKAGE

- MANUFACTURING INDUSTRY SUPPORT PACKAGE

- OPERATING EXPENSES SUPPORT PACKAGE FOR 6 FEBRUARY EARTHQUKES

- INVESTMENT SUPPORT PACKAGE FOR 6 FEBRUARY EARTHQUAKES

- SUPPORT PACKAGE FOR SEVERANCE PAYMENT OF RETIREMENT AGE VICTIMS

- REGIONAL SME SUPPORT

- SUPPORT PACKAGE FOR ACTIVITIES GENERATING FX-BASED INCOME

- SUPPORT PACKAGE FOR WOMEN ENTREPRENEURS

- ENTREPRENEUR SUPPORT PACKAGE

- SUPPORT PACKAGE FOR GREEN TRANSFORMATION AND ENERGY EFFICIENCY

- TECHNOLOGY SUPPORT PACKAGE

- SUPPORT PACKAGE FOR DIGITAL TRANSFORMATION

- EDUCATIONAL SUPPORT PACKAGE

- ACTIVE SUPPORT PACKAGES(2022)

- Other >

- Export Support Package

- Cold Air Units And Frigorific Vehicles Support Package

- Investment Support Package

- Additional Employment Support Package

- Manufacturing Based Import Substitution Support Package

- (KOBI DEGER LOANS)

- Treasury Fund (32,5 Billion TL)

- Treasury Fund (52,5 Billion TL)

- Treasury Fund (200 Billion TL)

- EKONOMI DEGER LOANS

- (KOBI DEGER LOANS II)

- TOBB NEFES LOAN 2020 SUPPORT

- ACTIVE SUPPORT PACKAGES(2023)

- Our Supports

- Information Center

- Press

- Contact Us

WHAT IS KGF?

KGF acts as a guarantor for SMEs and non-SME enterprises that cannot get a loan due to insufficient collateral. KGF supports SMEs and non-SME enterprises in access to financing.

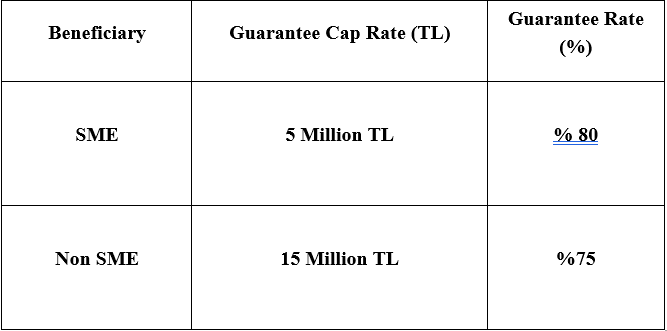

SUPPORT PACKAGE FOR OPERATING EXPENSES

Product Description

This package is aimed at providing SMEs and non-SMEs with financial support for all fixed expenses, including salaries and rental payments, thus ensuring they can healthily maintain their activities

Resource for Guarantee

Treasury Fund

Related Financial Institutions / Corporations

Akbank, Albaraka Türk Katılım Bankası, Denizbank, Emlak Katılım Bankası, Garanti Bankası, Halkbank, İş Bankası, Kuveyt Türk Katılım Bankası, QNB Finansbank, Şekerbank, Türkiye Finans Katılım Bankası, Vakıfbank, Vakıf Katılım Bankası, Yapı Kredi Bankası, Ziraat Bankası, Ziraat Katılım

Product Maturity

Maximum 24 months including a grace period of a maximum of 6 months

Guarantee Cap Rate and Guarantee Rates

Loan Products Available

- Business Credit Cards

- New Credit Card allocation

- Working capital loans that are to be disbursed to create a positive balance after making payments (including the following months) to a new Credit Card or existing Credit Cards that have no risk balance (Installment Loan, Spot Loan, Usury, etc.).

- Connected to a Debit/Bank Card;

- Overdraft Account (even if the beneficiary already has an account, a new overdraft account specific to this program must be opened)

- Installment Loan, Spot Loan, Usury, etc.

- Working Capital Loan / Usury (*)

- Installment Loan

- Spot Loan

- Revolving Loan

- Cashless Overdraft Account products

- Other approaches suitable for Participation Banking

* Participation Banks may disburse loans through appropriate methods for participation banking, regardless of Debit/Business Card.

Fee and Commission Rates

- The KGF shall collect, in return for each guarantee it gives, a one-time commission corresponding to 0.5% of the respective guarantee amount from the beneficiaries through the lenders. In the event of debt restructuring, a commission amounting to 0.5% of the balance amount of the guarantee shall be collected in advance from the beneficiaries through creditors.

- In retun for each loan disbursed, creditors may collect a commission amounting to a maximum of 1% of the loan amount from the beneficiaries.

Special Conditions

- Beneficiaries are required to commit to not reducing the number of employees for a period of two years from the date of loan disbursement

- Beneficiaries may receive, for use as operating expenses, a cash amount of not more than 10% of the working capital loan allocated to them.

- Credit cards will be restricted for cash advances

- Invoices related to loans to be used under this Package shall be checked through the Invoice Register System, except for: loans to be used for the payment of salaries, taxes, SSI premiums, rental fees, electronic product bills (ELUS), producer receipts, and invoices other than e-Invoice and e-Archive invoices; the cash portion of loans; loans to be made available through card payment systems; and loans disbursed to beneficiaries who have a certifying letter from the Defense Industries Agency (SSB) stating that the respective company is operating in the defense sector.

- Invoices related totreasury-backed guarantees shall be checked through the “Invoice Register System” created for Treasury-backed guarantees based on the invoice register systems of the Financial Institutions Association and the Participation Banks Association of Türkiye.

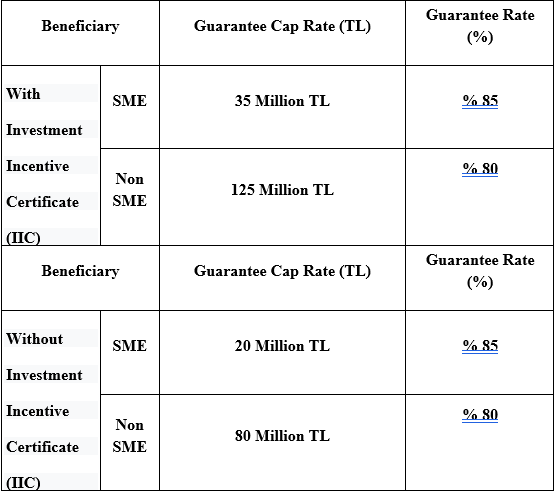

INVESTMENT-PROJECT FINANCE SUPPORT PACKAGE

Product Description

This package is aimed at providing financing for the investment and investment-related operating expenses of SMEs and non-SMEs that plan to invest, including those operating in the manufacturing industry and targeting export markets.

Resource for Guarantee

Treasury Fund

Related Financial Institutions / Corporations

Albaraka Türk Katılım Bankası, Denizbank, Garanti Bankası, Halkbank, İş Bankası, Kuveyt Türk Katılım Bankası, QNB Finansbank, Türkiye Finans Katılım Bankası, Türkiye Sınai Kalkınma Bankası, Kalkınma Yatırım Bankası, Vakıfbank, Vakıf Katılım Bankası, Yapı Kredi Bankası, Ziraat Bankası, Ziraat Katılım

Product Maturity

Investment Loan -Maximum 120 months maturity (including the grace period)-Maximum 24 months grace period

Working Capital Loan - -Maximum 36 months maturity (including the grace period)-Maximum 6 months grace period

Kefalet Limiti ve Kefalet Oranları

Loan Products Available

- Business Credit Cards

- New Credit Card allocation

- Working capital loans that are to be disbursed to create a positive balance after making payments (including the following months) to a new Credit Card or existing Credit Cards that have no risk balance (Installment Loan, Spot Loan, Usury, etc.).

- Connected to a Debit/Bank Card;

- Overdraft Account (even if the beneficiary already has an account, a new overdraft account specific to this program must be opened)

- Installment Loan, Spot Loan, Usury, etc

- Working Capital Loan / Usury (*)

- Installment Loan

- Spot Loan

- Revolving Loan

- Cashless Overdraft Account products

- Other approaches suitable for Participation Banking

-

Investment Loan (**)

* Participation Banks may disburse loans through appropriate methods for participation banking, regardless of Debit/Business Card.

** This support package allows debtors who use investment loans under this package to access additional working capital loans not exceeding 10% of the respective investment loan, provided that the working capital loan is disbursed by the same creditor.

Fee and Commission Rates

- The KGF shall collect, in return for each guarantee it gives, a one-time commission corresponding to 0.5% of the respective guarantee amount from the beneficiaries through the lenders. In the event of debt restructuring, a commission amounting to 0.5% of the balance amount of the guarantee shall be collected in advance from the beneficiaries through creditors.

- In retun for each loan disbursed, creditors may collect a commission amounting to a maximum of 1% of the loan amount from the beneficiaries.

Special Conditions

- Beneficiaries are required to commit to not reducing the number of employees for a period of two years from the date of loan disbursement

- Beneficiaries may receive, for use as operating expenses, a cash amount of not more than 10% of the working capital loan allocated to them.

- Credit cards will be restricted for cash advances.

- Beneficiaries may take out a working capital loan within the package, aside from the investment loan limit.

- Guarantees for investments in land and buildings can only be given if the investment includes machinery, aside from in the tourism sector.

- The amount of an investment loan cannot exceed 70% of the total investment planned or committed to by the enterprise. If the beneficiary has an Investment Incentive Certificate (IIC), the amount of the investment loan cannot exceed 70% of the total investment indicated on the IIC.

- For Investment Incentive Certificates obtained after 01.01.2022, the limit to be allocated to a beneficiary will be determined according to the limits for “SMEs and non-SMEs holding an Investment Incentive Certificate”.

- Invoices related to loans to be used under this Package shall be checked through the Invoice Register System, except for: loans to be used for the payment of salaries, taxes, SSI premiums, rental fees, electronic product bills (ELUS), producer receipts, and invoices other than e-Invoice and e-Archive invoices; the cash portion of loans; loans to be made available through card payment systems; and loans disbursed to beneficiaries who have a certifying letter from the Defense Industries Agency (SSB) stating that the respective company is operating in the defense sector.

- Invoices related totreasury-backed guarantees shall be checked through the “Invoice Register System” created for Treasury-backed guarantees based on the invoice register systems of the Financial Institutions Association and the Participation Banks Association of Türkiye.

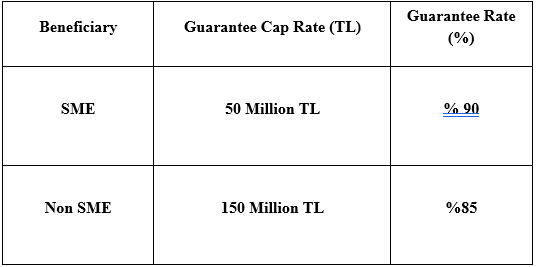

MANUFACTURING INDUSTRY SUPPORT PACKAGE

Product Description

It is aimed to facilitate the access to finance of all SMEs and non-SMEs operating in the following sectors: machinery manufacturing, electrical-electronics, manufacturing of electronic components and circuit boards, manufacturing of electric motor-generators and equipment, manufacturing of wires and cables used in cabling, pharmaceutical and medical companies, automotive supply industry, manufacturing of chemical, glass and soil industries (investments only for green transformations) and rail freight transportation (investments into electric locomotives).

Resource for Guarantee

Treasury Fund

Related Financial Institutions / Corporations

Albaraka Türk Katılım Bankası, Denizbank, Garanti Bankası, Halkbank, İş Bankası, Kuveyt Türk Katılım Bankası, QNB Finansbank, Kalkınma Yatırım Bankası,Türkiye Finans Katılım Bankası, Vakıfbank, Vakıf Katılım Bankası, Yapı Kredi Bankası, Ziraat Bankası, Ziraat Katılım

Product Maturity

Investment Loan -Maximum 120 months maturity (including the grace period)-Maximum 24 months grace period

Working Capital Loan - -Maximum 48 months maturity (including the grace period)-Maximum 12 months grace period

Guarantee Cap Rate and Guarantee Rates

Loan Products Available

- Business Credit Cards

- New Credit Card allocation

- Working capital loans that are to be disbursed to create a positive balance after making payments (including the following months) to a new Credit Card or existing Credit Cards that have no risk balance (Installment Loan, Spot Loan, Usury, etc.).

- Connected to a Debit/Bank Card;

- Overdraft Account (even if the beneficiary already has an account, a new overdraft account specific to this program must be opened)

- Installment Loan, Spot Loan, Usury, etc

- Working Capital Loan / Usury (*)

- Installment Loan

- Spot Loan

- Revolving Loan

- Cashless Overdraft Account products

- Other approaches suitable for Participation Banking

-

Investment Loan (**)

- Installment Loan

- Other approaches suitable for Participation Banking including Finance Lease

* Participation Banks may disburse loans through appropriate methods for participation banking, regardless of Debit/Business Card.

** Within the scope of this support package, beneficiaries using investment loans can use a business loan, provided that they are from the same lender, in addition to the investment loan, not exceeding 25% of the investment loan they use

Fee and Commission Rates

- The KGF shall collect, in return for each guarantee it gives, a one-time commission corresponding to 0.5% of the respective guarantee amount from the beneficiaries through the lenders. In the event of debt restructuring, a commission amounting to 0.5% of the balance amount of the guarantee shall be collected in advance from the beneficiaries through creditors.

- In retun for each loan disbursed, creditors may collect a commission amounting to a maximum of 1% of the loan amount from the beneficiaries.

Special Conditions

- Beneficiaries are required to commit to not reducing the number of employees for a period of two years from the date of loan disbursement

- The amount of an investment loan cannot exceed 70% of the total investment planned or committed to by the enterprise. If the beneficiary has an Investment Incentive Certificate (IIC), the amount of the investment loan cannot exceed 70% of the total investment indicated on the IIC.

- Beneficiaries may receive, for use as operating expenses, a cash amount of not more than 10% of the working capital loan allocated to them.

- Credit cards will be restricted for cash advances.

- Invoices related to loans to be used under this Package shall be checked through the Invoice Register System, except for: loans to be used for the payment of salaries, taxes, SSI premiums, rental fees, electronic product bills (ELUS), producer receipts, and invoices other than e-Invoice and e-Archive invoices; the cash portion of loans; loans to be made available through card payment systems; and loans disbursed to beneficiaries who have a certifying letter from the Defense Industries Agency (SSB) stating that the respective company is operating in the defense sector.

- Invoices related totreasury-backed guarantees shall be checked through the “Invoice Register System” created for Treasury-backed guarantees based on the invoice register systems of the Financial Institutions Association and the Participation Banks Association of Türkiye.